Law360 is providing free access to its coronavirus coverage to make sure all members of the legal community have accurate information in this time of uncertainty and change. Use the form below to sign up for any of our weekly newsletters. Signing up for any of our section newsletters will opt you in to the weekly Coronavirus briefing.

Sign up for our California newsletter

You must correct or enter the following before you can sign up:

Thank You!

Law360 (April 21, 2020, 4:27 PM EDT ) Venture capital financings in Silicon Valley surged in January but suffered a steep drop-off once the coronavirus hit the U.S., with a report from Fenwick & West released Tuesday showing that VC fundings in the region fell significantly between January and March.

The data come from Fenwick & West LLP's Silicon Valley Venture Capital Flash Report for the First Quarter of 2020, which was authored by Cynthia Clarfield Hess, Mark Leahy, Barry Kramer and Khang Tran. Hess and Leahy are both corporate partners and co-chairs of Fenwick's startups and venture capital group, while Kramer is a corporate partner emeritus and Tran is a corporate knowledge and innovation attorney.

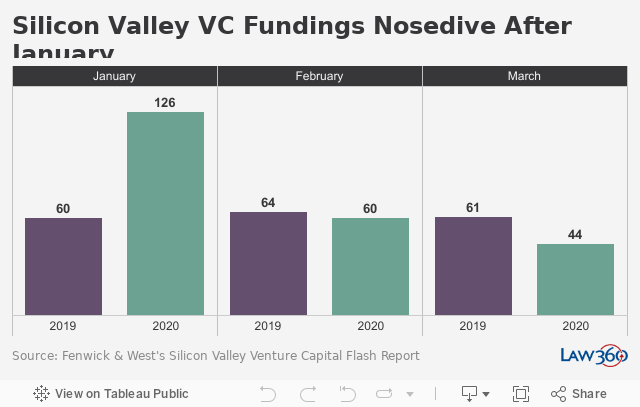

The report looks at priced equity financings of companies headquartered in Silicon Valley that raised at least $1 million from venture capitalists or other professional investors during the applicable time period. It shows that there were 126 VC financings in Silicon Valley during January, which represents the largest number of venture financings in a single month in at least half a decade and more than double the amount of VC financings as in January 2019.

Click to view interactive version

However, the numbers dropped back down in February and March, with 60 and 44 VC financings in those months, respectively. The report notes that it's possible the firm will still learn of a few more March 2020 financings due to delayed reporting.

According to Leahy, while there's no way of knowing exactly why the numbers look the way they do, there are some reasonable guesses. For instance, December was fairly slow, with only 54 financings, so perhaps the explosion in January was a little bit of a catch-up. But no matter how you slice it, there's no question that the global pandemic had an impact.

"As we got deeper into January, it was clear there were problems with the coronavirus in China," Leahy told Law360. "Clients were anxious how that was going to affect their supply chains and customer demand. Then [the virus] started spreading into Europe, and companies started getting anxious about how much business overall was going to be affected."

By March, people in the U.S. were being told by the government at both the state and local levels that they should stay home in order to flatten the curve, making it even clearer that the business world was not going to escape the health crisis unscathed.

"I don't think any of us expected the shelter-in-place orders," Leahy said. "Clients were worried about the impact in general on the world economy. And boards started telling companies to be careful about how they were spending their cash."

Fenwick's data show that there was a notable decline in financing price increases as the first quarter progressed. In January, the average price for a venture financing round compared to its prior round was up 117%, but that number declined to 76% in February and 46% in March. As a frame of reference, the average price increase in financings completed in March 2019 compared to the prior round was 63%.

"People were saying, 'Let's go ahead and close some rounds that we otherwise maybe would have held off on and not closed until later in the year,'" Leahy said.

Additionally, the firm noted that there was no significant change in non-price terms during the first quarter, which is unusual for an economic downturn.

"During past significant economic downturns we have typically seen an increase in terms like senior/multiple liquidation preference, ratchet anti-dilution and pay-to-play provisions," the report said. "These terms will bear watching in the coming months."

Although he admits that he, just like everyone else, is merely playing a guessing game, Leahy said he is optimistic that, because the underlying economic conditions are stronger now than they were when the 2008 financial crisis hit, the negative effects won't be as long-lasting.

"This was a government-mandated economic shutdown," he said. "When the government starts pulling it off — and maybe I'm an optimist — life might spring back quicker than it did in 2008. Maybe investors will be optimistic sooner than they were in 2008 to start making investments. We just don't know yet."

--Editing by Alanna Weissman.

For a reprint of this article, please contact reprints@law360.com.