Law360 is providing free access to its coronavirus coverage to make sure all members of the legal community have accurate information in this time of uncertainty and change. Use the form below to sign up for any of our weekly newsletters. Signing up for any of our section newsletters will opt you in to the weekly Coronavirus briefing.

Sign up for our Capital Markets newsletter

You must correct or enter the following before you can sign up:

Thank You!

Law360 (July 31, 2020, 11:32 AM EDT ) The private equity industry has not been insulated from the effects of the coronavirus pandemic, but fund managers are learning to navigate the market with strategies like targeting special purpose acquisition vehicles and distressed assets to pave the way for a much more active second half of the year.

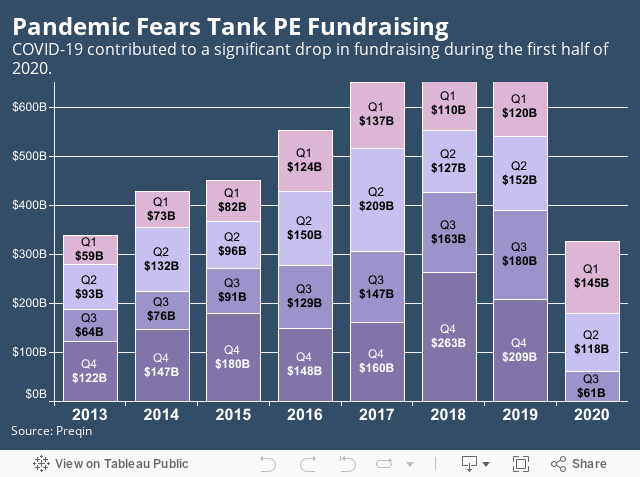

Private equity dealmaking and fundraising were both hit hard by COVID-19 during the first half of the year. In the second quarter, there were 929 PE-backed buyouts worth a total of $68.4 billion, which represents the lowest volume and value for such deals in a single quarter since at least 2013, according to data provided by research firm Preqin.

When it comes to fundraising, meanwhile, the second quarter saw 260 total fund closings worth a total of $118.35 billion. That volume of funds is the lowest since at least the first quarter of 2013, per Preqin, while the total value is the lowest since the first quarter of 2018.

While the second half of the year hinges on whether or not another wave of COVID-19 cases again forces widespread business closures, experts anticipate dealmaking and fundraising to rebound. Even if the pandemic persists, experts say fund managers and their attorneys have been finding creative ways to work around shutdowns and are now better prepared to continue being active in a world where people work remotely.

"We're seeing new deals in the marketplace, both from strategic buyers and PE buyers," said Rahul Patel, a partner at King & Spalding LLP and co-chair of the firm's global private equity and mergers and acquisitions practice. "People are adapting, and while ultimately it is difficult to do a deal 100% virtual, buyers and sellers are starting to do more virtually, including virtual site visits using drones."

Here, Law360 explores five ways private equity clients are adapting to the post-COVID-19 landscape.

PE Sponsors to Lean on SPACs

Special purpose acquisition companies, or SPACs, also known as blank check companies, have been growing in popularity for a while now, and the pandemic has only escalated the trend.

"There's an old quote: 'Victory has 1,000 fathers, but defeat is an orphan,'" said Dan Clivner, a partner at Sidley Austin LLP and global co-leader of the firm's M&A and private equity group. "SPACs now have 1,000 fathers."

SPACs are shell entities that raise money through initial public offerings in order to acquire a private company and take it public. They are often led by private equity investors or business executives with expertise in a specific industry who look for underperforming companies with potential for increased value. Through June 15, there were 31 blank-check IPOs that raised $9.8 billion compared with 26 such IPOs that raised $5.9 billion at this time last year, according to Dealogic data — 65% more in proceeds compared with 2019's pace. And more deals are lining up.

"More recently, you're seeing a lot more sponsors backing SPACs," said Mehdi Khodadad, a partner at Sidley Austin whose practice is focused on private equity, M&A and capital markets with an emphasis on the technology and life sciences sectors. "It's a hot space. We're seeing more activity, and people don't want to miss the train."

Dealmakers to Look for Distressed Assets

The virus made it difficult for many businesses to survive, especially those in industries like retail, hospitality and transportation, but there hasn't been a resulting rash of distressed M&A yet. That's likely to change as the end of the year nears, according to Patel.

There are multiple reasons for the delay in distressed M&A activity, including that some struggling companies have received government relief and lenders have been willing to work with borrowers during the early stages of COVID-19. At some point, though, government rescue packages may not be able to sustain businesses for the long term and lenders will run out of flexibility, meaning borrowers will have to turn to other options.

"People are certainly preparing for it," Patel said.

For private equity firms to get in on a potential distressed M&A bonanza, they'll require more than just the cash they have on hand and the capital they've raised for funds; they'll need to be able to tap into the debt financing markets, which have taken a hit in the wake of the outbreak.

"You may see more activity from strategics who have the ability to tap available cash," Patel said. "For PE to really kick in, the debt financing markets have to open up more."

But the availability of debt financing is likely to remain subdued until there is more certainty in what the future will hold for the M&A market at large.

"Uncertainty is always the enemy of deals," Patel said.

Deal Terms Likely to Feature Earnouts

In many cases, companies that have still sought to pursue deals in the uncertain environment caused by the pandemic are building in earnout provisions. That means there will be less upfront cash and more deferred payments, giving the buyer the ability to wait on having to pay the entire purchase price. It should come as no surprise to attorneys that earnout provisions, as well as clauses denoting that some portion of the price tag is contingent upon the achievement of future milestones, are becoming increasingly popular.

"Clients are trying to price in the risk that comes with economic uncertainty by having more contingent consideration and earnouts, with less cash up-front," said Alison Johnson, a M&A partner at Holland & Hart who counsels businesses and venture capital firms.

That being said, lawyers must beware of the potential pitfalls of relying on earnouts and similar provisions in deal agreements.

"Most lawyers and clients grossly underestimate the optionality and complexity of earnouts," Clivner said.

If not very specifically negotiated, earnouts can lead to "irrational conduct, such as accelerating revenues or deferring expenses in order to hit the targets that need to be reached so that the full consideration will be paid, Clivner said.

"In order to protect against that, these provisions need to be fully negotiated," Clivner said. "You can't just do a simple earnout pasted into the agreement."

A mishandled earnout clause can lead to a lawsuit down the line, so it's important for attorneys to negotiate conditions for how the business must be run in the years after the deal has been inked so that no funny business can occur, Khodadad said. Without precise language in earnout provisions, headaches can occur for both sides.

"There's always potential for gamesmanship with earnouts," Khodadad said. "You have to be really careful about how you draft them."

More Firms Eyeing Opportunistic Funds

Fund managers have noticed that the statistics show a dip in overall fundraising, and attorneys should be prepared for PE clients to adjust their strategies to meet the current environment. Just as it's believed that an uptick in distressed M&A is inevitable, lawyers should expect an increase in funds with an investment mandate specifically focused on opportunistic investments or special situations.

Not every fund manager will launch an entirely new fund targeting such opportunities; some are tweaking the mandates of funds that already exist to give them the ability to switch gears and take advantage of opportunities that may present themselves in the coming months. Gilman pointed to real estate and retail as areas that were especially hard hit by the economic shutdown, and are therefore ripe for the picking by opportunistic PE players.

"We have seen a significant increase in the number of clients seeking to pursue opportunistic or market dislocation strategies, either by establishing new bespoke investment products or by utilizing some of the available capital in their existing flagship funds," said Peter Gilman, a corporate partner at Simpson Thacher & Bartlett LLP.

Add-On Deals to Outpace Platform Acquisitions

Even before the pandemic, add-on deals were becoming an increasingly popular deal type, and the trend has only accelerated in the wake of the COVID-19 outbreak. Add-on acquisitions are smaller transactions that serve to bolster a firm's portfolio company without necessarily shelling out for huge multiples.

Fund managers have become fond of such deals in recent years because they often present better opportunities to build value and make more money down the line when the time comes for an exit. Boosting the value of a more established platform-type asset is far more difficult than doing so for a smaller business. Add-ons, on the other hand, can be integrated with other similar businesses the PE firm owns in order to create value.

Right now, however, the reason add-ons are all the rage is a little more simple, according to Brian Richards, a partner in Paul Hastings LLP's private equity and M&A practices and chair of the firm's global PE practice.

"Add-ons can get done," Richards said.

That's because there is typically a management team at the platform company that knows the industry well, meaning there isn't the usual learning curve that comes with buying a business in an area that a fund manager doesn't have much experience with. Additionally, lenders are more willing to provide financing for smaller add-on deals, as they'll have more confidence in the management team's ability to make the transaction successful.

"Lenders want to put money out," Richards said. "That's their job. But, like buyers, you have to be able to predict demand. Even as the country starts to open up, we don't know if things will ultimately go back to where we were in April."

--Additional reporting by Tom Zanki. Editing by Alanna Weissman and Sarah Golin.

For a reprint of this article, please contact reprints@law360.com.